Shell 2Q24 Results | Climate Transition Insights

This report comprises general statements of factual information and not financial advice. Read our Important Notice.

Shell’s 2Q results saw significant developments in LNG, contributing to approximately half of its 20-30% sales growth ambitions. While Shell continues to frame LNG as a decarbonisation lever, its impact will be minimal. Set-backs in biofuels highlight a broader issue with Shell’s strategy; Shell will struggle to meet its emission intensity target without a material use of offsets and divestments.

Our view

Shell’s current strategy falls short of ambition. To deliver real emission reductions, Shell needs to raise capex ambitions for low-carbon, increase its focus on transitioning customers away from oil to low-carbon, and move away from its reliance on offsets to deliver targets.

Investors engaging with Shell should ask for:

1) Increase capital expenditure in low-carbon from FY26, moving towards 50% by FY30

2) Increase its focus on transitioning customers from oil to low-carbon, quantifying the use of divestments

3) Set boundaries on offsets, recognising their limitations and providing a breakdown of its offset portfolio

Key findings

-

In 2Q24, Shell expanded its LNG portfolio with a spate of new deals: acquiring Singaporean LNG trader Pavilion Energy (6.5 Mtpa contracted portfolio), securing 10% of Adnoc’s 9.6 Mtpa Ruwais LNG project in Abu Dhabi, and taking FID on the Manatee gas field in Trinidad and Tobago.

These investments align with Shell’s bullish LNG strategy put forward in its updated energy transition strategy, where Shell reiterated LNG is a ‘critical fuel in the energy transition’. Although Shell frames LNG as a decarbonisation lever, it has limited impact. Increasing the weighting of gas in Shell’s portfolio by 10% by FY30 will result in only a 4% reduction in net carbon intensity (with all else equal). The same increase in renewables would achieve a reduction of ~14%.

Shell justifies its aggressive LNG position by flagging expected strong demand growth led by Asia. The Pavilion acquisition in Singapore and the Ruwais investment align with this strategy. The Manatee deal aligns with Shell’s intention to focus on integrating LNG production with its upstream value chain, feeding into the Atlantic LNG plant. The company has not set upstream gas production targets, and LNG ambitions could mean an 8% to 16% growth by FY30.

Shell is targeting LNG sales growth of 20-30% between FY22-30. This translates to 67 Mtpa in FY23 to ~79-86 Mtpa by FY30. Adnoc and Pavilion alone could account for ~40%-60% of additional volumes at peak.

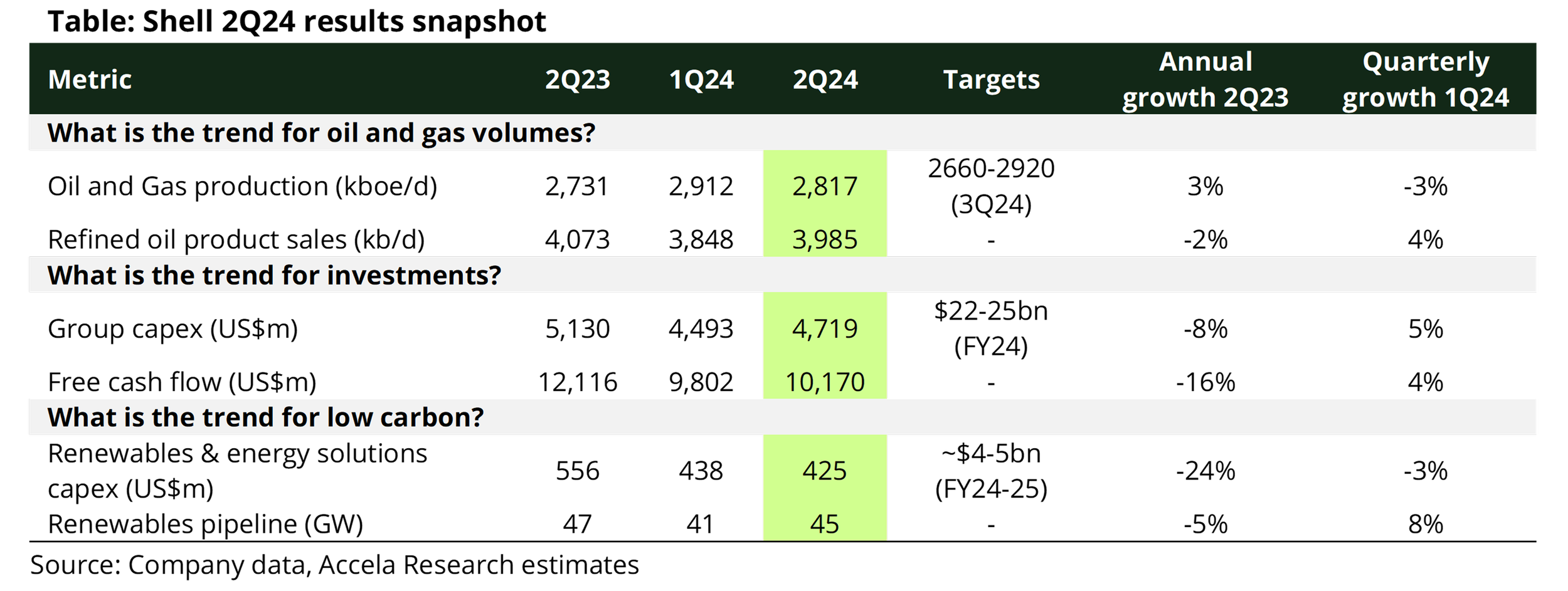

Despite 2Q24 group capex falling 8% from 2Q23, Integrated gas rose 6% to $1.2bn, 24% of total capex, the highest proportion of spending in the last 10 quarters.

-

This quarter Shell paused construction at its biofuels facility in Rotterdam due to technical considerations, reporting a post-tax impairment of $783m in Marketing. The delays in Rotterdam appear to be project-specific, but they highlight a broader issue with Shell’s strategy; Shell will struggle to meet its emission intensity target without a material use of offsets and divestments.

Shell's ambition to reduce refined oil product emissions and its target to grow LNG sales will only lead to a ~1% decline on Net Carbon Intensity (NCI). The company has already dialled back its focus on renewables. With Rotterdam and a struggling biofuels environment, Shell will have limited options moving forward.

If we continue to see biofuel delays, Shell might run out of available levers to reach Net Carbon Intensity targets outside of divestments and offsets. Last year, 20 Mt of offsets accounted for ~50% of Net Carbon Intensity reductions, allowing Shell to reach their FY23 target. If Shell intends to use power to decarbonise, the company would need to sell the electricity generated from ~88 GW of renewable capacity, either from the company or from third-parties, to reach the upper end of its FY30 NCI target without relying on additional offsets.

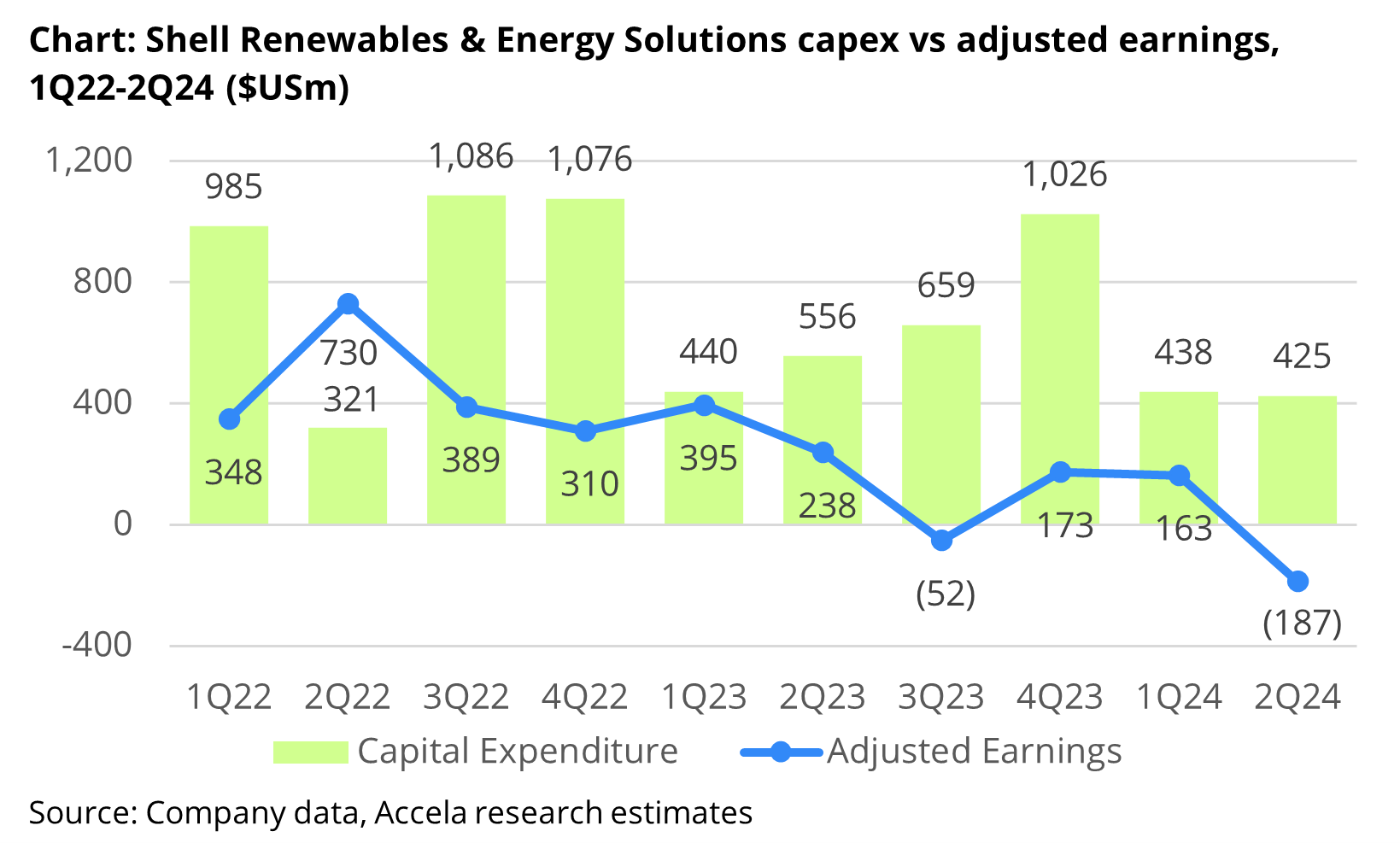

Shell is the lowest among peers for FY25 low carbon capex ambition at ~20% of group capex. 2Q24 saw a 24% decrease in Shell’s Renewables & Energy Solutions capex to $425m.

-

In 2Q24, Capex continued the decline seen in 1Q, falling $400m from 2Q23 to $4.7bn, an 8% reduction. This was materially driven by a -$200m decrease in Upstream (-10% on 2Q23) and a -$131m decrease in Renewables & Energy solutions (-24% on 2Q23). Shell confirmed its group capex guidance of $22-25bn for FY24.

Shell’s oil and gas production grew 3% to 2.82 M boe/d from 2Q23, driven by a 5% uptick in the Upstream segment from new oil delivery in Deepwater. The company guided to 2.66-2.92 M boe/d for 3Q23.

Adjusted earnings grew $1.2bn from 2Q23 to $6.3bn, an increase of 24%. This was materially driven by stronger performance in Upstream, which grew 38% to $2.3bn. Renewables & Energy Solutions struggled, posting a loss of $187m compared to adjusted earnings of $238 in 2Q23 due to weaker performance in trading and commodity prices.

Shell maintained buybacks of $3.5bn to be completed in 3Q24. The company reported 43% of CFFO distributed over the last 12 months, exceeding its guidance of 30-40%.