BP 2Q24 result | Climate Transition Analysis

This report comprises general statements of factual information and not financial advice. Read our Important Notice.

2Q24 results indicate that BP is at a crossroads, facing a choice between advancing its transition plans and providing short-term shareholder returns.

Our view

We see BP as a leader in the transition to low-carbon energy due to its ambition and progress so far in building low-carbon offerings. However, recent developments in 2Q raise concerns about this momentum. BP has scaled back its low-carbon initiatives, coupled with a 14% decrease in capital expenditure and up to a 29% reduction in earnings for its Transition Growth Engines in the first half of FY24. The question now is how BP manages the balance between advancing its transition plans and providing short-term shareholder returns.

Investors engaging with BP should ask for:

1) Clarity on BP’s trade-off between shareholder distributions (committed to at least $14bn between FY24-25) and low carbon investment, with BP targeting up to ~50% ($6-8bn) group capex for TGEs by FY25, up from 23% in FY23.

2) Greater quarterly disclosure on earnings and capex for low carbon business (EV charging, biofuels, renewables & power, hydrogen) to assess transition performance.

3) Better disclosures relating to divested assets. Divestments are likely to continue as a key lever towards its absolute scope 3 target, with 200 kboe/d of capacity flagged for sale by FY30.

4) Emissions reduction strategies and targets linked to its customer sectors, to drive real world emissions reductions and enable more productive engagement on transition

Key findings

-

BP is at a crossroads, facing a choice between advancing its transition plans and providing short-term shareholder returns.

2Q results saw BP raise its dividend 10% and announce a $1.75bn buyback for 3Q24, reiterating guidance for $3.5 billion in the second half of 2024. The company plans at least $14 billion in share buybacks through FY25, returning at least 80% of surplus cash flow to shareholders.

BP also responded to investor pressure over the quarter with dial backs across multiple low carbon offerings. In June, the company announced a renewables hiring pause and slowed low-carbon investments. In hydrogen, the company flagged it is high-grading its pipeline from 30 opportunities to 5 to 10 potential projects this decade. BP’s hydrogen pipeline has declined 11% to 2.5 Mt pa from 1Q24.

In Bioenergy, BP flagged a key priority moving forward will be a “simpler, more focused and higher value company”; refocusing its portfolio by announcing its acquisition of full ownership of Bunge, while scaling back plans to develop biofuels projects in Germany and the U.S.

These moves come after CEO Murray Achincloss’ comments in 1Q, which emphasised the company's commitment to prioritising returns over volume in the coming years, and also hinting at more oil and gas in FY30 than its prior guidance.

Despite the strategic shift seen over 2Q, the company asserts its “destination remains unchanged”. By FY30, BP is targeting ~10 GW of renewable capacity (50 GW to FID), 0.5-0.7 Mtpa of hydrogen production, ~100 kb/d biofuels production, and ~70 kboe/d biogas supply.

-

BP's new ‘simplified’ approach was evident in the numbers this quarter, with TGEs capex and earnings struggling. There is now a real question if BP will deliver on the investment needed to fund its low carbon volume targets.

BP reported 1H24 Transition Growth Engines capex at $1.8bn, down 14% from 1H23. BP needs to double this rate of investment to achieve its $6-8bn by FY25. Hitting this target will be crucial for the company’s transition plan; at a minimum, we estimate BP will need to invest $8bn p.a between FY25-30 to achieve its low carbon volume ambitions.

The company reported 1H24 Transition Growth Engines EBITDA of $0.5bn in, down 29% from 1H23 ($0.7bn). This included $0.3bn for bioenergy, $0.5bn convenience, $0.1bn renewables & power, and losses in EV charging (-$0.1bn) and Hydrogen (-$0.2bn). Earnings will have to significantly ramp-up by FY25, with BP reaffirming its target of $3-4bn, including ~$2bn from bioenergy, and >$1.5bn for Convenience & EV charging.

Moving forward, BP’s ability to deliver on low-carbon will be linked to its financial position nearer-term. We saw some improvement with net debt falling $1.4bn from 1Q to $22.6bn, and estimated surplus cash flow returning to the green at ~$2.5bn.

-

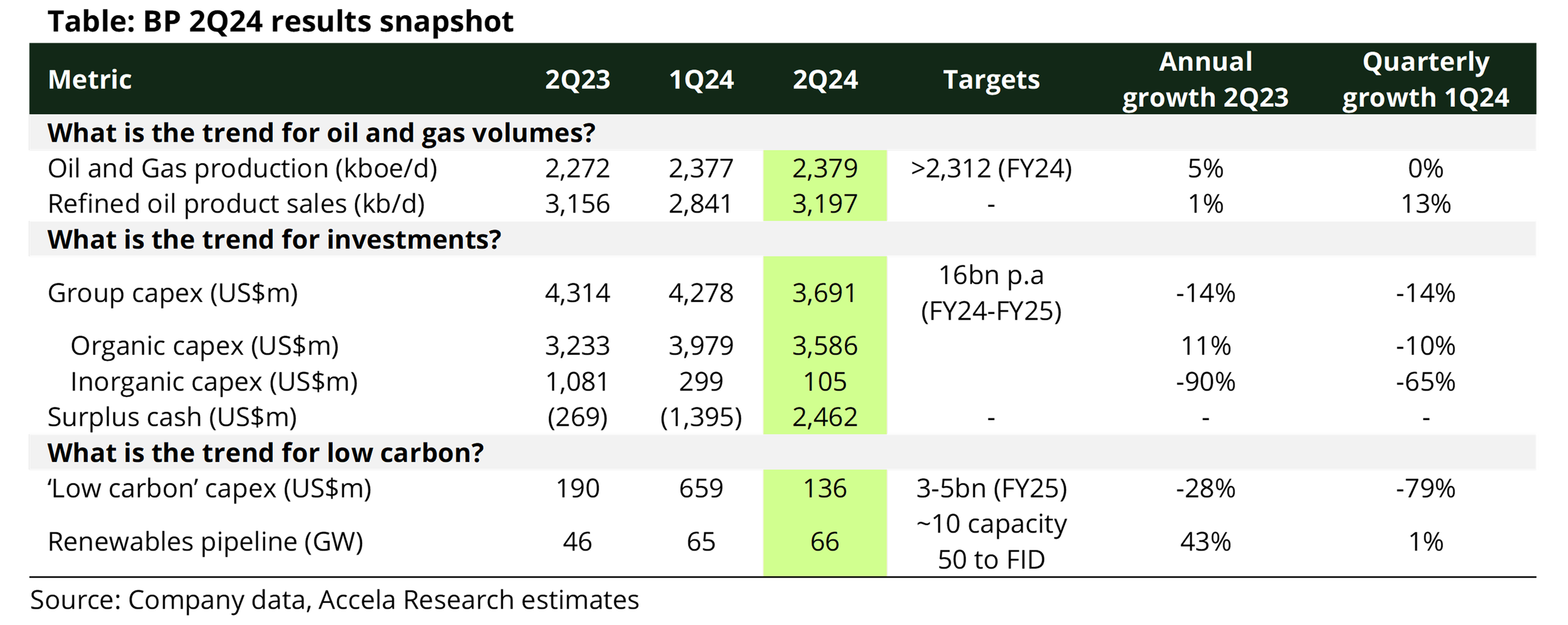

In 2Q24, BP’s oil and gas production grew 5% to 2.38 mboe/d compared to 2Q23, due to increased production in the oil production and operation segment . Despite 3Q, production expected to be lower, the company is still guiding to slightly higher production in 2024 than 2023 (~2,312kboe/d).

Capex declined 14% from 2Q23 to $3.7bn, with this drop driven by a 90% reduction in inorganic capex. Total capex for 1H24 is now ~$8bn, with capex guidance for 2024 unchanged at $16bn.

Group underlying profits before interest and tax was down 3% on 2Q23. A 37% reduction was recorded in gas-low carbon earnings driven by a lower average gas marketing and trading result.

The company will provide an update on its medium term plans in February. This will include details on capital allocation and oil and gas production plans in the second half of the decade. We expect the update could be more reflective of BP’s decision to slow momentum in low-carbon.

Next update on emissions to be provided in early 2025.