Eni 2Q24 Results | Climate Transition Analysis

This report comprises general statements of factual information and not financial advice. Read our Important Notice.

This quarter we saw Eni’s ‘Satellite model’ in action, signing an exclusivity agreement with KKR for the sale of a 20-25% stake in its Enilive business.

Our view

Eni claims funding growth through its satellite model will provide access to additional capital markets, but we haven’t seen any evidence of this. With the company lagging peers in low-carbon capex ambition, the question will be whether Eni will use divestment proceeds to increase low-carbon capex guidance or to fund higher distributions.

Either way, it needs more money than it has guidance to build the low-carbon business. We estimate that to meet its renewable generation targets it will need an additional ~€2bn in capex by 2030.

Investors engaging with Eni should ask for :

1) Whether Eni’s satellite model will lead to higher low carbon investment than already guided, to bring ambition in line with peers.

2) A quantified breakdown of decarbonisation levers. Eni has the most ambitious absolute targets compared to peers, aiming for a -35% reduction in net scope 1, 2, & 3 emissions between FY18-30. However, its target may be at risk, with plans to increase oil and gas production by up to 15% by FY30, the highest of its European peers.

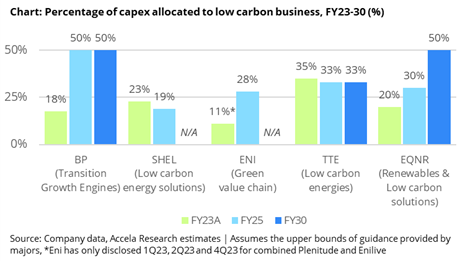

3) Increased ambition for low-carbon investment. Eni’s short-term capex guidance is ~28% of group, placing its ambition only ahead of Shell. In addition, the company does not provide low-carbon capex guidance to FY30.

4) Match Net Carbon Intensity (NCI) ambition with peers. Eni’s FY30 NCI target is the least ambitious compared to peers at -15% between FY19-30 (vs -19%-20%).

Key findings

-

In 2Q24, Eni’s oil and gas production grew 6% on 2Q23. This growth was driven by a ramp-up in flagship projects, higher contributions from Libyan assets, and the full integration of Neptune Energy. As a result, the company is now guiding towards the upper range of its FY24 guidance of 1.69 to 1.71 mboe/d. Eni has the most aggressive oil and gas strategy of the Euromajors, guiding to a 15% increase between FY23-30.

Despite the production increase, Eni’s adjusted net-profit was down 21% to €1.52bn. The decline was largely due to a 77% decrease in earnings from Eni’s Global Gas and LNG portfolio to €185m due to lower prices and volatility together with one-off negotiations/settlements in 2Q23.

Capex was down 21% on 2Q23 to €2.02 bn, due to a 38% reduction in capex for Exploration & Production. In contrast, low-carbon capex for Eni’s Enilive and Plenitude segment increased by 108% on 2Q23 to €397m.

Eni is engaged in a divestment strategy to high grade its upstream portfolio, targeting €2bn of net divestments annually between FY24-27. Due to greater-than-anticipated progress in its divestment plan and the resulting proceeds, the company now expects group capex net of acquisitions/divestments to be under €6bn for FY24, a downgrade from the previous guidance of €7-8bn. In 2Q, key announcements included Eni’s UK oil and gas portfolio, onshore Nigerian assets, and upstream assets in Alaska.

-

Earnings from Eni’s Enilive and Plenitude segments were down 34% to €143m, including €66m for Enilive and €77m for Plenitude. Earnings decline was materially driven by Enilive (-52% from 2Q23) due lower biofuel margins in the quarter.

Renewable installed capacity grew marginally to 3.1 GW, up 24% from 2Q23 but only 3% from the previous quarter. The company confirmed its target to reach 4 GW of installed capacity for FY24, meaning installed capacity will need to grow on average 14% for the next 2 quarters.

A similar ramp-up will be needed for EV charging. EV charge points grew 23% from 2Q23 to 20,400, but only 4% from the previous quarter. With the company targeting 24,000 charge points by FY24, Eni will need to grow its network 8% per quarter for the remainder of the year.

The company confirmed Enilive and Plenitude adjusted pro-forma EBITDA (including equity share contributions) guidance of €1bn for both businesses in FY24. Notably, the majority of Plenitude earnings (80%) will come from Plentitude’s retail business, which engages in gas, power, and services marketing to retail/business clients.

-

Eni’s satellite model should give it an advantage in funding the transition, but today, despite having the best absolute emissions targets, Eni lags behind its peers.

In 2Q, the company announced an exclusivity agreement with KKR for the sale of a 20-25% stake in its Enilive business, raising €2.5-3bn. This deal follows on from Eni’s €600m sale of a 9% stake in Eni’s Plenitude business in March to Equity Infrastructure Partners.

Eni claims funding growth through its satellite model will provide access to additional capital markets, but we haven’t seen any evidence of this. Although we saw an increase in Plentitude & Enilive capex for 2Q24, it currently stands at 15% of the group in 1H24, and the company spent less on low carbon than peers in the last year (disclosing 11% vs peers 23%). Eni’s short-term low carbon capex guidance is expected to reach just 28% of the group, behind BP (50%), TTE (33%), and Equinor (50%). Additionally, the company provided no guidance for FY30.

The question will be whether Eni will use divestment proceeds to increase low-carbon capex guidance or to fund higher distributions. Either way, it needs more money than it has guidance to build the low-carbon business. We estimate that to meet its renewable generation targets it will need an additional ~€2bn in capex by 2030.