TotalEnergies 2Q24 Results | Climate Transition Analysis

This report comprises general statements of factual information and not financial advice. Read our Important Notice.

TotalEnergies once again demonstrated the successful build-out of its Integrated power segment in 2Q. Adjusted net operating income for the segment was $502m, up 12% from 2Q23. The company has now surpassed earnings of $500m for the last 4 quarters for the segment.

Our view

2Q24 results once again showed that TotalEnergies’ low-carbon build-out is head and shoulders above peers, but its medium-term oil and gas growth strategy to 2030 continues to hold it back from securing the top spot of transition strategies.

TotalEnergies has a peer leading renewables pipeline and a promising Integrated Power business showing signs of profitability. However, the company has one of the most aggressive oil and gas growth strategies behind Eni, and the least ambitious emissions targets alongside Equinor compared to peers. For this quarter, investors engaging with TotalEnergies should ask for:

1) A move away from reliance on offsets, CCS and divestments to achieve scope 1 & 2 target.

2) Guidance and ambition for the electrification of gas clients within their Integrated Power portfolio

3) Quarterly disclosures for its Low-carbon Molecules business, to track progress against its Low Carbon Energies (Integrated Power + Low-carbon Molecules) capex target of 33% group spend.

Key findings

-

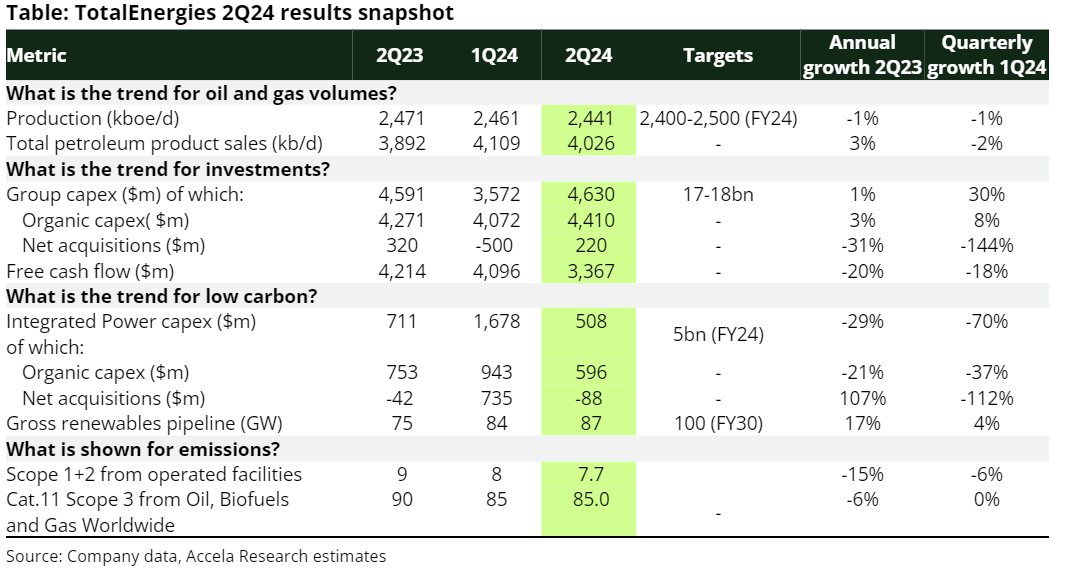

TotalEnergies once again demonstrated the successful build-out of its Integrated power segment in 2Q. Adjusted net operating income was $502m, up 12% from 2Q23. The company has now surpassed earnings of $500m for the last 4 quarters for the segment, which has accounted for 10% of group earnings for 1H24. Its gross renewables pipeline now sits at 87 GW, up 17% from 2Q23, with the company targeting 100 GW of operational capacity by FY30.

2Q24 renewable power capacity hit 24 GW, up 2% from the previous quarter. This is more than the entire combined capacity of Shell, BP, Equinor and Eni combined at ~11 GW. Despite its impressive record, the company will need to ramp up operational capacity 8% per quarter to meet its 28 GW target by FY24, and further maintain 6% growth over FY25 to meet its 35 GW target.

In hydrogen, the company acquired a 50% stake in a 795 MW offshore wind farm in the Netherlands to produce 40kt/yr of green hydrogen. It also signed a 15-yr agreement with Air Products for the delivery of 70kt/yr of green hydrogen starting in 2030. Under both deals, TotalEnergies will use the hydrogen to decarbonise its refineries.

TotalEnergies continues to have a gap in quarterly disclosures. It does not provide disclosures on Low-carbon Molecules capex, making it challenging to track its progress against its Low Carbon Energies (Integrated Power + Low-carbon Molecules) capex target of 33% group spend.

We want the company to follow steps taken by its peer Eni who established a new reporting segment in Q1 for Enilive & Plenitude (Eni’s equivalent to TotalEnergies’ Low-carbon Energies business).

-

TotalEnergies’ Integrated LNG segment struggled in 2Q.

In Integrated LNG, TotalEnergies reported a 13% decline in adjusted net operating income for 2Q24 to $1.2bn from 2Q23, and a 30% drop between 1H23-1H24. The company cited lower LNG prices and sales, including a 20% reduction in 2Q24 LNG sales to 8.8 Mt, and a 24% decline in LNG production to 7.6 Mt.

Despite the results, Integrated LNG capex surged 40% from 2Q23 to $822m. This included the purchase of a 20% stake in the Texas Dorado Gas field, which will increase gas production by 50 Mcf/d and contribute to LNG production in the US. There were additional significant moves in LNG totaling 3 Mtpa - with Marsa LNG, Ruwais and 2 signed Indian contracts - which will enter the portfolio later in the decade.

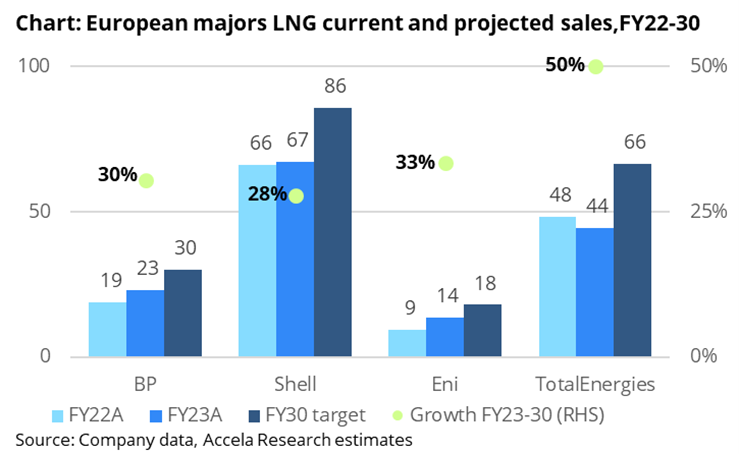

Like Shell, TotalEnergies views LNG as a decarbonisation lever, but we estimate TotalEnergies' LNG ambitions will have less than 1% impact on its NCI by FY30.

TotalEnergies targets ~66 Mtpa LNG equity and offtake by FY30, up from 44 Mtpa in FY23, second only to Shell's 86 Mtpa. In terms of growth, TotalEnergies’ ambition surpasses all peers with expected growth of 50% between FY23-FY30, ahead of Eni (33%), BP (30%), and Shell (28%).

-

In 2Q, group capex was up 1% on 2Q23 to $4.63 bn. Reductions in capex were recorded for the Integrated Power segment (-29% on 2Q23) and refining and chemicals (-35%). The company confirmed capex guidance of $17-18bn for FY24, including $5bn in Integrated Power.

Production was 2.44 Mboe/d, down 1% from 2Q23 due to higher planned maintenance in the North Sea. For 3Q, the company guided towards production between 2.4 and 2.49 Mboe/d with the start of the Anchor project in the Gulf of Mexico due in 3Q.

Adjusted net operating income was down 4% on 2Q23, driven by reduced earnings from the marketing and services segments (-16%), integrated LNG (-13%), but most significantly refining and chemicals (-36%). This was due to lower refining margins mainly in Europe and the Middle East.

Scope 1 and 2 operational emissions were down 15% on 2Q23, and 1H24 emissions are now 15.9 Mt CO2e (-13% on 1H23).This reduction is due to decreased flaring emissions at E&P facilities and lower utilization of gas-fired plants in Europe due to reduced gas demand. While this is positive progress, the overall impact on TTE’s annual 2024 emissions will depend on whether a continuous decline in flaring emissions can offset increased gas demand as Europe enters colder seasons.