Eni 1Q24 Results | Climate Transition Analysis

Eni’s 1Q24 results introduced a new low-carbon segment, with the company now reporting the consolidated performance of its Plenitude and Enilive business.

Our view

It is promising to see Eni’s new consolidated segment for Plenitude & Enilive, which will enhance the tracking of its low-carbon performance. However, there remains to be a disconnect between Eni’s absolute emissions targets, which are the most ambitious of European peers, and its projected growth of fossil fuels.

Investors engaging with Eni should ask for

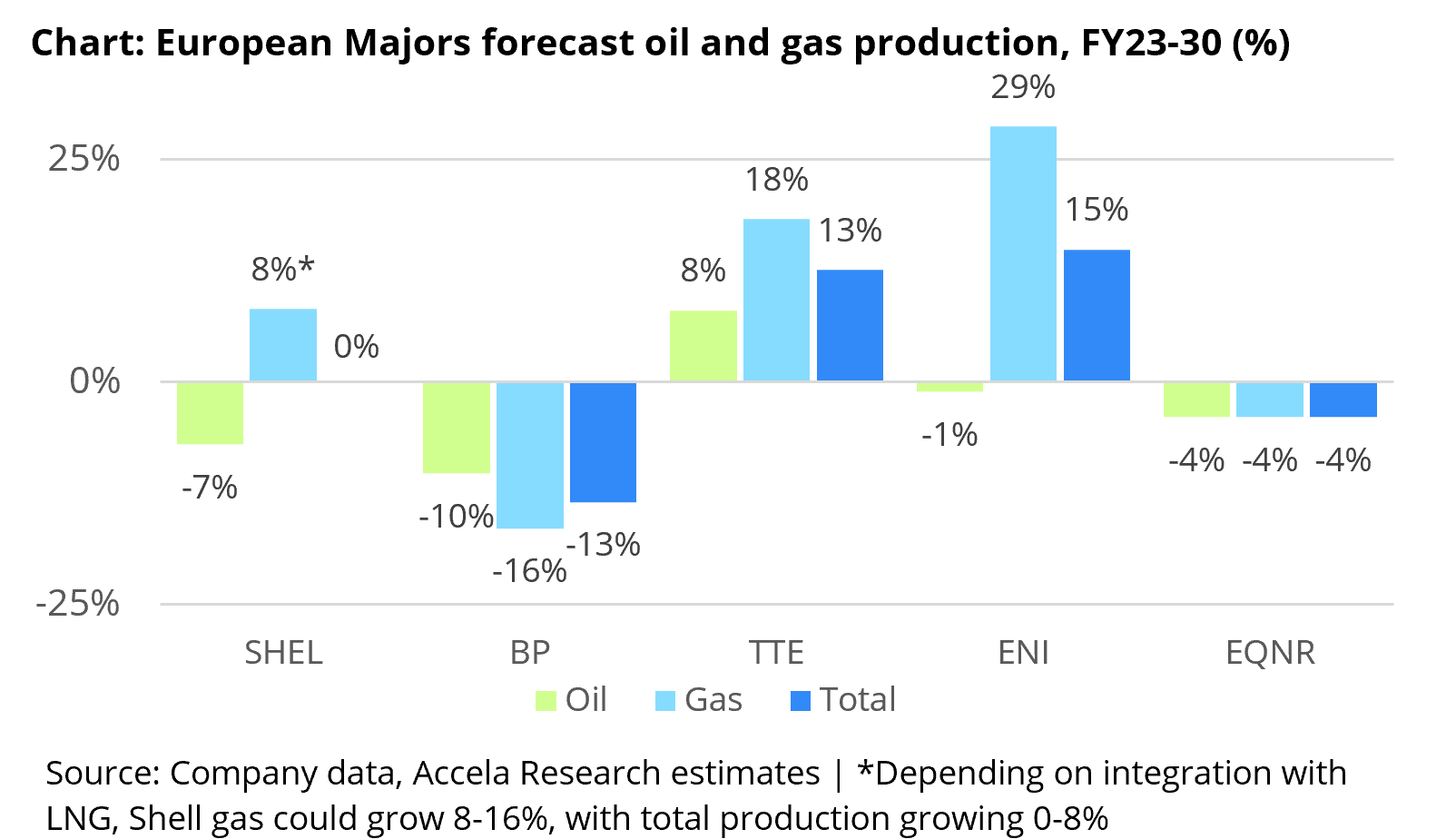

1) A quantified breakdown of decarbonisation levers. Eni has the most ambitious absolute targets compared to peers, aiming for a -35% reduction in net scope 1, 2, & 3 emissions between FY18-30. However, its target may be at risk, with plans to increase oil and gas production by up to 15% by FY30, the highest of its European peers.

2) Increased ambition for low-carbon investment. Eni’s short-term capex guidance is ~28% of group, placing its ambition only ahead of Shell. In addition, the company does not provide low-carbon capex guidance to FY30.

3) Match NCI ambition with peers. Eni’s FY30 NCI target is the least ambitious compared to peers at -15% between FY19-30 (vs -19%-20%).

Key findings

-

It was great to see Eni address a critical gap we had previously identified by establishing a new reporting segment for Enilive & Plenitude (see our view on Eni). Prior to 1Q24, Plenitude was grouped with Power (Eni’s gas generation business) and Enilive with refining and chemicals. This change provides visibility for the first time into the adjusted net profit for both Plenitude and Enilive and the capex allocated to Enilive.

Low-carbon capex was up 16% from 1Q23 to €205m, including €33m in Enilive and €172m in Plenitude. The company has guided towards annual net capex of €0.5bn for Enilive and €1.4bn for Plenitude between FY24-28.

Group capex was down 9% from 1Q23 to €1.9bn. The company confirmed net capex guidance of €7-8bn for FY24.

-

The group’s adjusted net profit almost halved on 1Q23, down -46% to €1.58bn.

Earnings declined across every segment except Enilive & Plenitude, which was up 57% from 1Q23 to €288m. For Enilive, the company cited higher bio-throughputs from capacity additions and wholesale demand. For Plenitude, earnings benefitted from higher electricity margins and renewable capacity additions.

Low-carbon earnings outperformed Eni’s Global Gas & LNG Portfolio segment, which was down 80% to €204m and accounted for 60% of the group’s earnings decline. The company cited weak commodity prices and trading results.

Despite the significant decline in earnings, Eni announced it plans to raise its FY24 buy-back by 45% to €1.6 bn, previously €1.1bn.

-

Eni demonstrated significant progress within its Plenitude business in 1Q24. EV charge points grew 33% from 1Q23 to 19,600, with the company targeting 24,000 charge points by FY24.In addition, renewable energy generation rose 12% from 1Q23, reaching 1.11 TWh.

Renewable installed capacity remains at 3.0 GW, up 29% from 1Q23 but unchanged from the previous quarter. Eni confirmed its 4 GW target for FY24 and flagged an additional 2 GW of organic capacity currently under construction.

Despite this growth in low-carbon, Eni continues to pursue an aggressive oil and gas growth strategy. Production for the quarter was 1.74 M boe/d, up 5% from 1Q23 and outpacing the company’s 2% CAGR target. Eni’s growth ambitions place it firmly ahead of European peers, 15% between FY23-30.