Woodside: Not delivering on decarbonisation

Woodside shareholders are about to vote on its climate plan, but there are doubts about what emissions reductions it will deliver.

In this insight, we take a closer look at Woodside's transition strategy, evaluating its climate performance and low carbon ambition compared to European Majors.

Our work finds that Woodside's proposed plan is trailing its peers across the board, with emissions forecast to rise with production, growing 16% to FY27.

Key takeaways:

When reviewing Woodside’s climate plan, investors need to consider the following:

-

We forecast Woodside’s scope 3 emissions will rise with production, growing 16% to FY27.

A sharp decline in sanctioned oil and gas production after FY27 means Woodside can decrease scope 3 emissions by displacing oil and gas with low carbon opportunities rather than contingent reserves.

-

Emissions targets address just 8% of total, compared to the European majors with absolute targets addressing 20-100% of emissions and net carbon intensity targets covering all emissions.

Woodside is also missing an opportunity to deliver real-world scope 1 and 2 reductions by FY30, with an estimated ~70% of reductions coming from offsets and only a minor 6% from efficiencies and renewables to address fuel consumption (70% of scope 1 & 2).

-

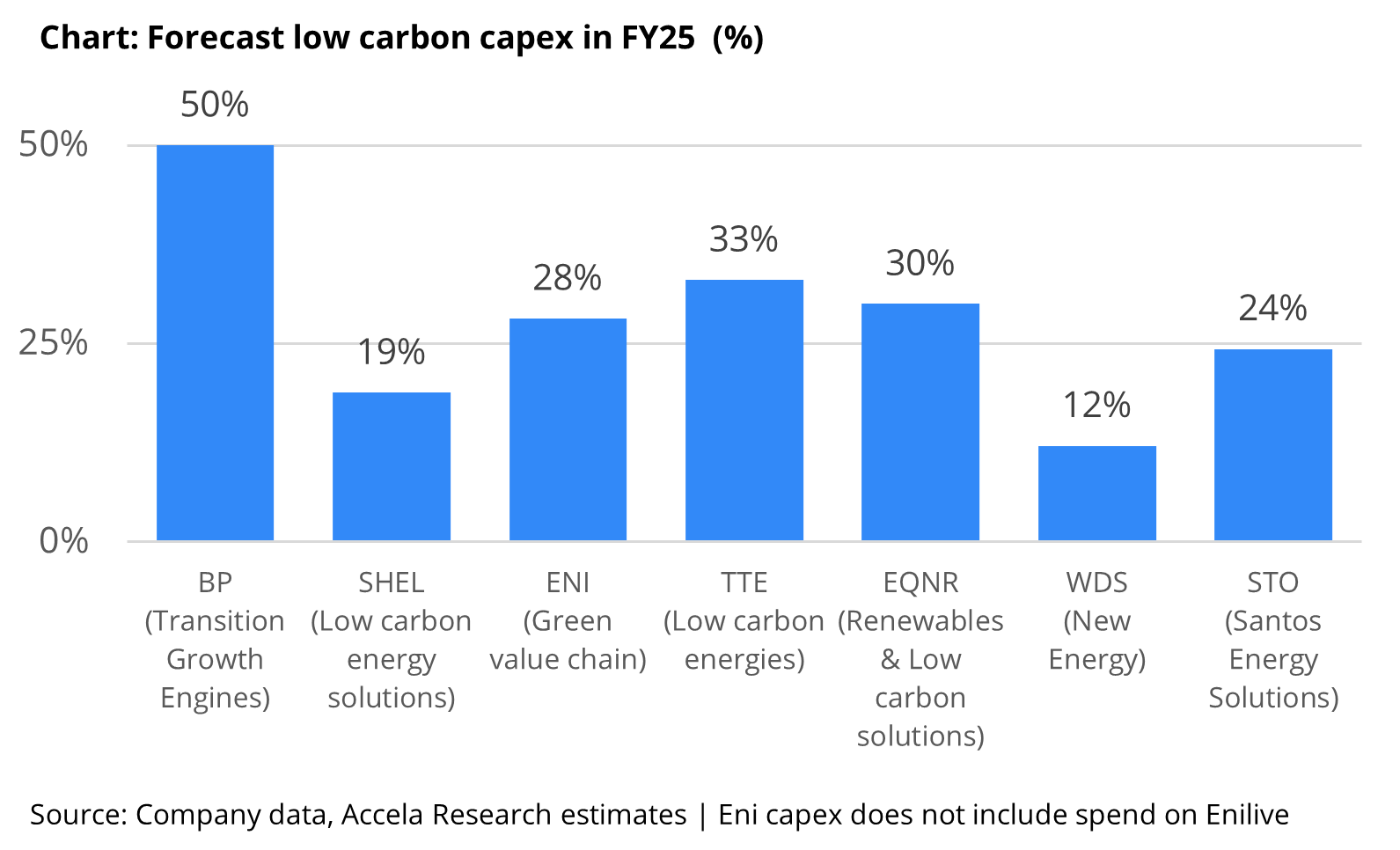

FY25 transition capex as a percentage of the group is ~20% less than European Majors, at 12% vs 32%. Additionally, despite a ramp-up of spend in New Energy ($335m FY22-23), investment must grow 26% pa. on average to FY30 to meet its $5bn aim.

The proposed 5Mtpa of emissions avoided or abated translates into an expensive and small opportunity, which if dedicated solely to hydrogen could equate to only 0.5 Mtpa of hydrogen at $10/kg (rel. to global average of $6.3-9.6/kg). Woodside has an opportunity to increase ambition as the projected cost for hydrogen is expected to halve by FY30.