Shell’s strategy is to remain reliant on offsets, questioning the sufficiency of low-carbon levers

Shell will hold a Say on Climate vote on its 2024 Energy Transition Strategy at its AGM on 21 May, but is its new plan ambitious enough?

In this insight, we look closer at Shell’s updated Energy Transition strategy, comparing its ambition to that of its European peer, BP and evaluating its key levers for emission reduction through FY30.

We find that Shell’s new transition strategy is better connected to its corporate strategy, but falls short of ambition to deliver real emission reduction.

To deliver an adequate transition plan Shell needs to close three critical gaps:

Raise its capex ambitions from FY26, moving to 50% by FY30.

Increase its focus to transition customers away from oil to low-carbon.

Set boundaries on the quantity and quality of offsets it relies on moving forward, with over 60 Mt of offsets estimated to be required based on its FY30 portfolio mix.

Key takeaways:

-

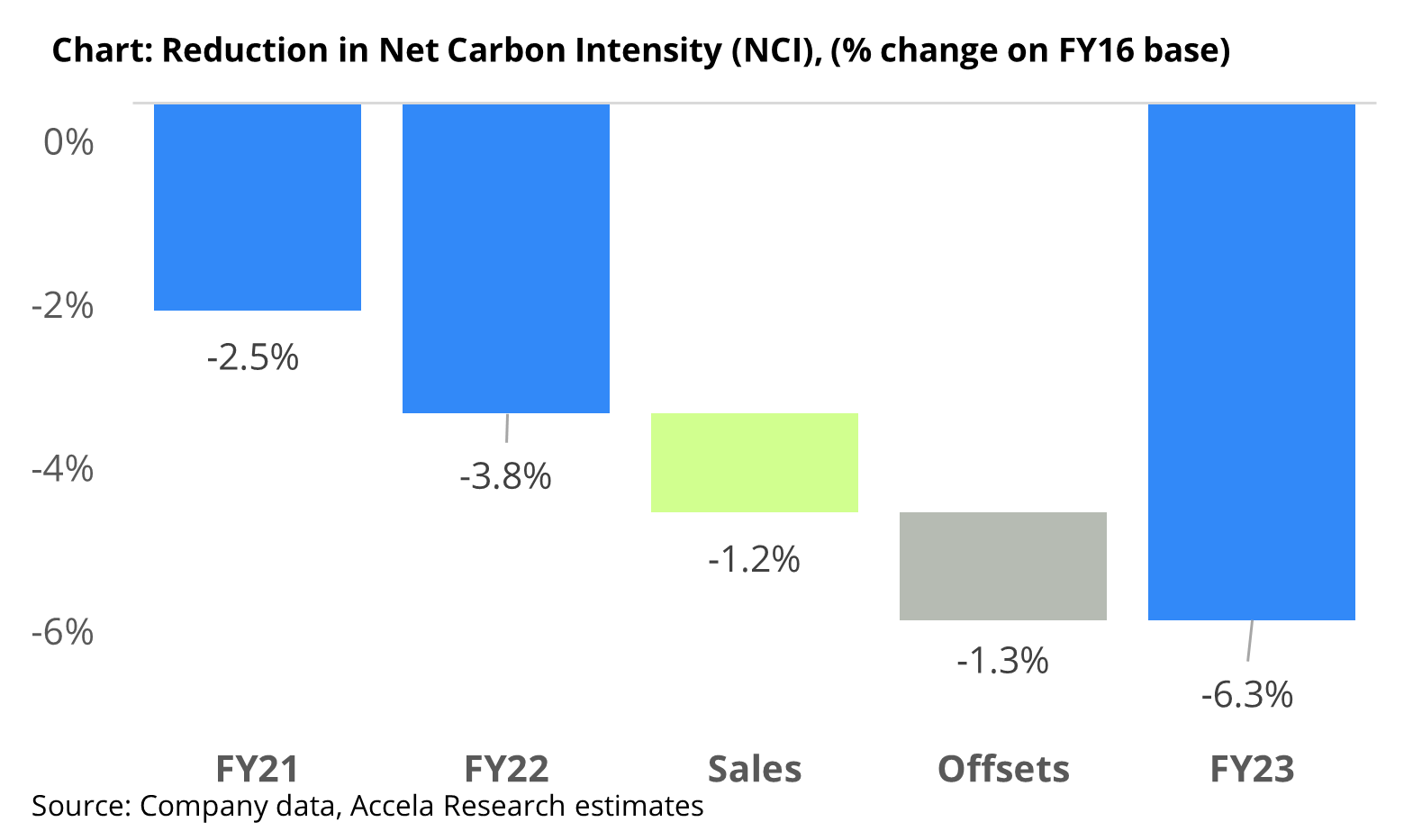

In FY23, Shell reported a 6.3% reduction in its net carbon intensity (NCI)(-15-20% target). With 20 Mt of offsets retired in FY23, we estimate that a third of Shell’s FY23 NCI progress came from offsets instead of selling lower-intensity fuels.

Moving forward, Shell’s new ambition to deliver a 15-20% reduction in scope 3 emissions from oil sales by FY30 (-9% achieved to date) will amount to only ~3-5% of FY23 scope 3 emissions.

Based on Shell’s newly disclosed FY30 portfolio mix, we estimate bioenergy and power will reach 14% of its mix by FY30 (from 9% today). To meet its FY30 NCI target with this mix, ~25% of NCI reductions will require offsets, even if the company’s electricity sales become 100% renewable by FY30. We estimate this is equivalent to offsets from a mature forest up to 3x the size of Denmark.

-

Across the Euromajors, Shell currently sells the most LNG (67 Mt) and this is projected to continue to FY30 between FY22-30 with the company targeting an increase of 20-30% for LNG sales (86 Mt pa) and 25-30% for LNG production (39 Mt pa).

Shell’s view of LNG as a “critical fuel in the energy transition” is now reflected in its annual bonus scorecard where its energy transition metric (15% weighting) includes a target for increased equity LNG (5% weighting). No other peers except TotalEnergies have included fossil fuel growth within their equivalent sustainability or low-carbon metrics.

-

Shell's new energy transition plan is centred on expanding its EV network, growing biofuels, and redirecting growth in power sales to commercial customers rather than retail customers. This ambition is underpinned by a single target to grow its public EV charging network to 200k by FY30.

By FY25, Shell plans to allocate an estimated ~ 19% of its capex to low-carbon initiatives. This is lower than peers, with BP planning to allocate ~50%, TotalEnergies 33%, Equinor 30%, and Eni 28% by FY25.

To align with IEA recommendations for the oil and gas industry to transition to net zero, Shell needs to significantly ramp up its capex ambitions post-FY25 to meet the recommended 50% by FY30.

-

As of FY23, Shell has outpaced BP in low-carbon capex by 1.5x, building a larger EV network (1.9 x), but trailing BP on its renewable capacity (0.9x), renewable pipeline (0.7x) and biofuels production (0.8x).

Moving forward to FY30, we find both companies have similar emission targets to FY30. Shell however has a more aggressive oil and gas strategy and lower ambition for establishing its low-carbon business.

In low-carbon, Shell’s FY24-25 guidance for low-carbon capex ($2.2-4.7bn) is 0.4-0.6x less than BP ($6-8bn). While, BP sets FY30 targets across multiple low-carbon offerings (renewables, biofuels, biogas sales and hydrogen production), Shell only sets a target for EV charging. Shell uses lower or comparable internal hurdle rates for low-carbon (Shell 12% vs BP >15% for EV charging and bioenergy, 6-8% for power/renewables) but BP’s EBITDA outlook is higher.

In oil and gas, Shell is expected to exceed BP in producing 1.4x oil, 1.4-1.5x gas and sell 2.9x LNG in FY30.