Shell 1Q24 Results | Climate Transition Analysis

Shell’s first quarterly result after the release of its 2024 Energy transition Strategy indicates a shift towards a more conservative approach to capital allocation.

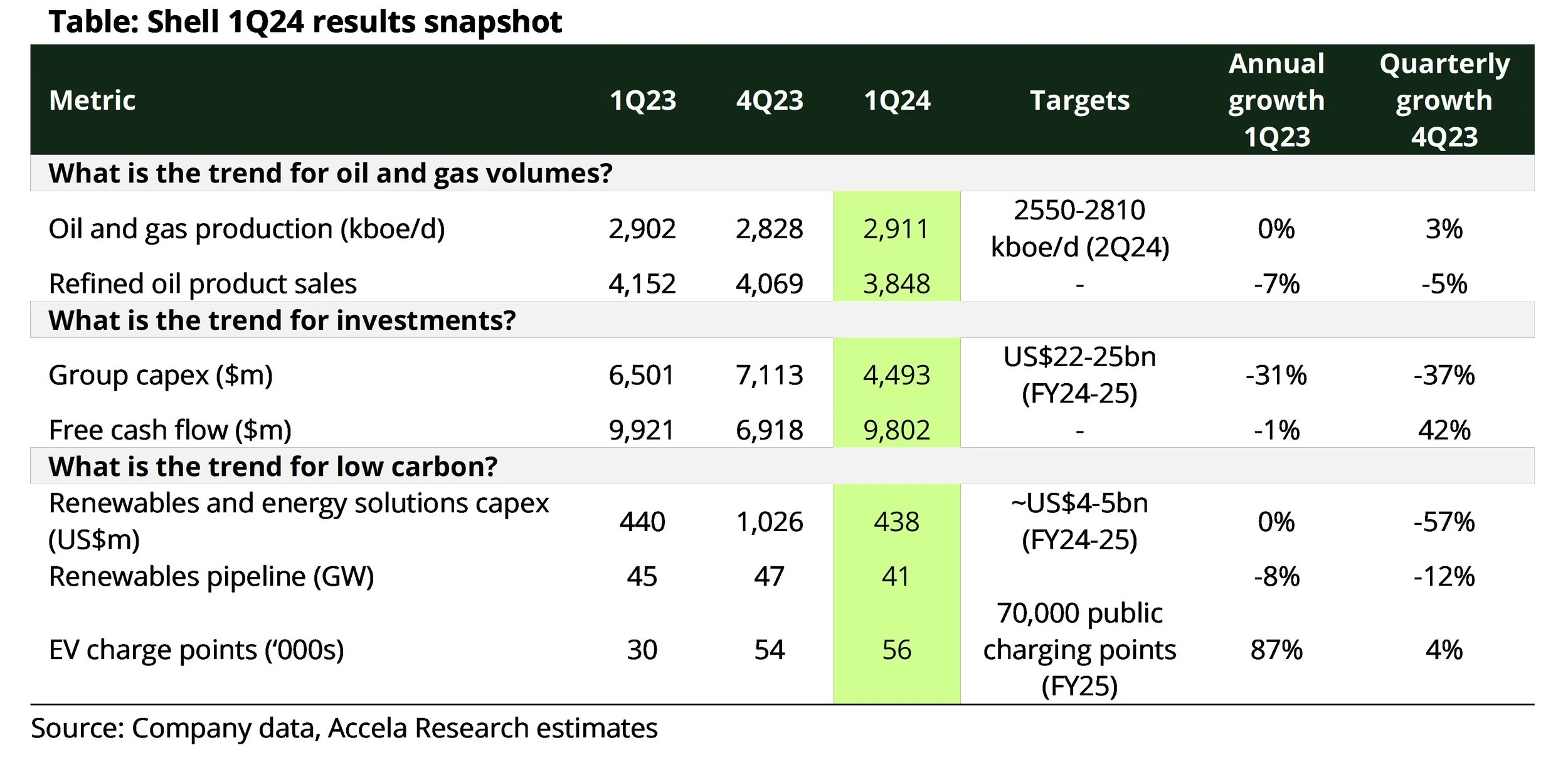

While group capex was down 31% on 1Q23, an increase in capex was observed in both the upstream and integrated gas segments.

Our view

Shell’s current strategy falls short of ambition. To deliver real emission reduction Shell needs to raise capex ambitions for low-carbon, increase its focus to transition customers away from oil to low-carbon, and move away from its reliance on offsets to deliver targets.

Key findings

-

Despite marginal change in free cashflow (-1% on 1Q23), group capex was reduced to its lowest in the past 8 quarters at $4.5 bn, down -31% on 1Q23. The biggest decline was in the Marketing segment (-83% on 1Q23), followed by Chemicals & Products (-11%). In contrast, capex in integrated gas was up 28% followed by Upstream (+7%).

Shell indicated that declines were driven by timing but also due to the implementation of capital discipline. The company reaffirmed cash capital expenditure for FY2024 within the range of $22 - $25 bn in line with guidance provided at its Capital Markets Day 2023.

With the company guiding to $10-15bn (~5bn p.a) capex in low-carbon energy solutions between FY23-25, we estimate this equates to ~19% of group capex in FY25, below the ambition of other European peers.

-

Group earnings were up 6% on 4Q23, but down 20% on 1Q23. Earnings declines in Integrated gas and Upstream were the main drivers.

Despite reduced earnings within Integrated gas, the company reiterated plans to grow its LNG sales 20-30% to 2030 (on FY22), with a view that LNG will be required for decades to come instead of being a short-term transition fuel.

Our latest analysis finds Shell will be selling the most LNG of majors to 2030. Combined with Shell’s ambition to reduce oil sales by 15-20% by 2030, the shift in the company’s portfolio will lead to a mere ~1% reduction in Net Carbon Intensity (NCI), with the company needing other low carbon levers to address the remaining 12% decrease in NCI by FY30.

-

Shell’s EV charging network has grown 87% since 1Q23 to 56k with the company making steady progress to meet its target of 70k charge points by FY25. In contrast, its renewable pipeline has declined 12%

In renewables, Shell remains focused on selectively participating in markets where it can leverage its competitive advantage in energy trading and optimisation rather than power generation. Within the quarter, Shell exited its China power generation and trading business as it did not believe it could hold a competitive advantage with its optimisation and trading capabilities. It also divested its 60% stake in Texas Brazos Wind Farm but secured 100% of the offtake to maintain its access to green electrons.